Bitcoin Blooms in the Autumn

Disclaimer: Your capital is at risk. This is not investment advice.

ATOMIC 101;

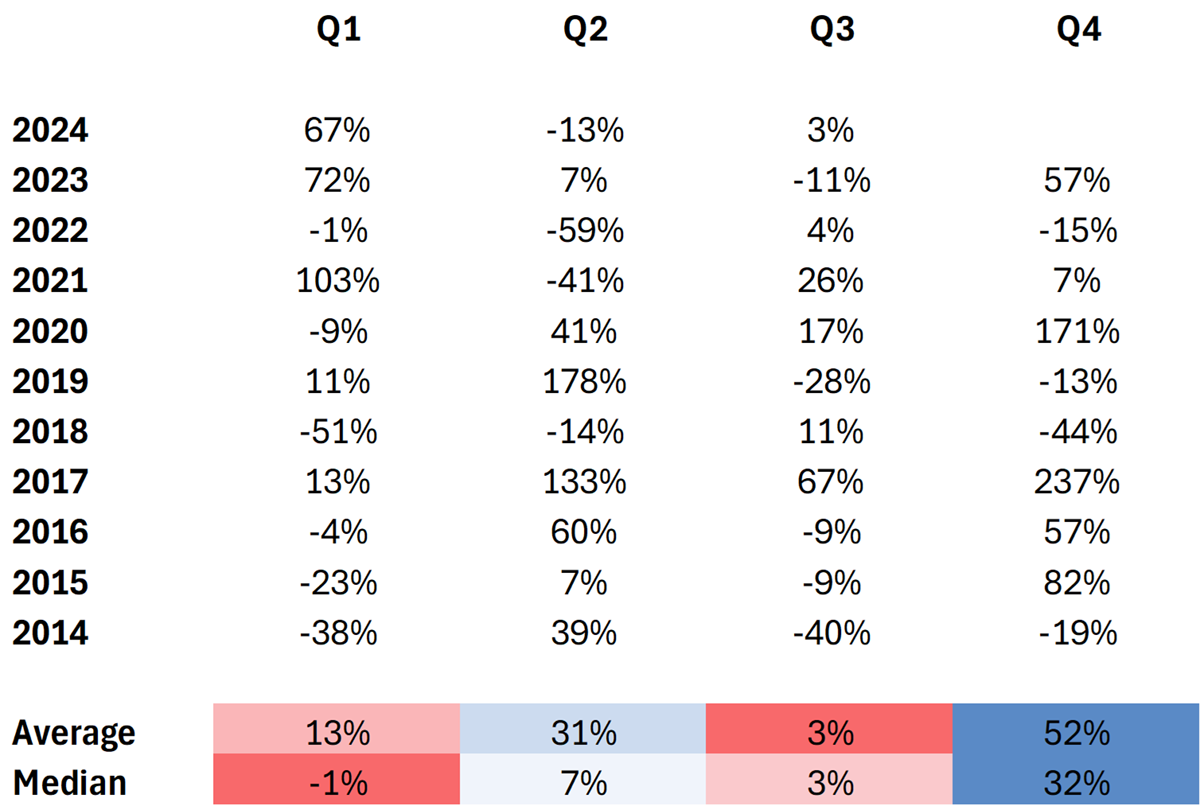

After a hot and dry summer on the blockchain, autumn is here. This is historically the season when Bitcoin blooms, with the highest average return by far, whether measured by median or mean.

ByteTree ATOMIC

Analysis of Technical, On-chain, Macro, Investment Flows and Crypto Stocks.

Highlights

| Technicals | Breaking the Bear |

| On-chain | Improving |

| Investment Flows | Neutral |

| Streaming | Gold Ordinals |

| Macro | Printer go Brrr |

| BOLD | New High and Fees Cut |

That said, the fourth quarter hasn’t always been kind to Bitcoin, as in 2018, it fell 44%.

Bitcoin Returns by Quarter USD %

At least Q4 2018 marked the end of a brutal bear market, in which the price of Bitcoin fell 83.2% from $19,041 to $3,156. The other bear year was 2014. Notice how October was not that bad, even in the bear years. And more often than not, it has hosted some spectacular rallies.

Bitcoin Performance in October, November and December over the past 10 Years

Seasonality is never something to bet the ranch on, but this October could be a good one. 2024 is a halving year, just like 2016 and 2020. Both times saw a summer lull followed by an autumn surge.