Lower Rates Lead to Real Estate

Trade in Soda;

I recently added the long bond to the Soda Portfolio as evidence that inflation was calming enough to stabilise the bond market. Inflation may have been cooling for two years, but the bond market was still in the turbulence of the hikes of 2022. It seems 5% is enough for anyone these days, and with public deficits going out of fashion, government bonds may even honour their commitments.

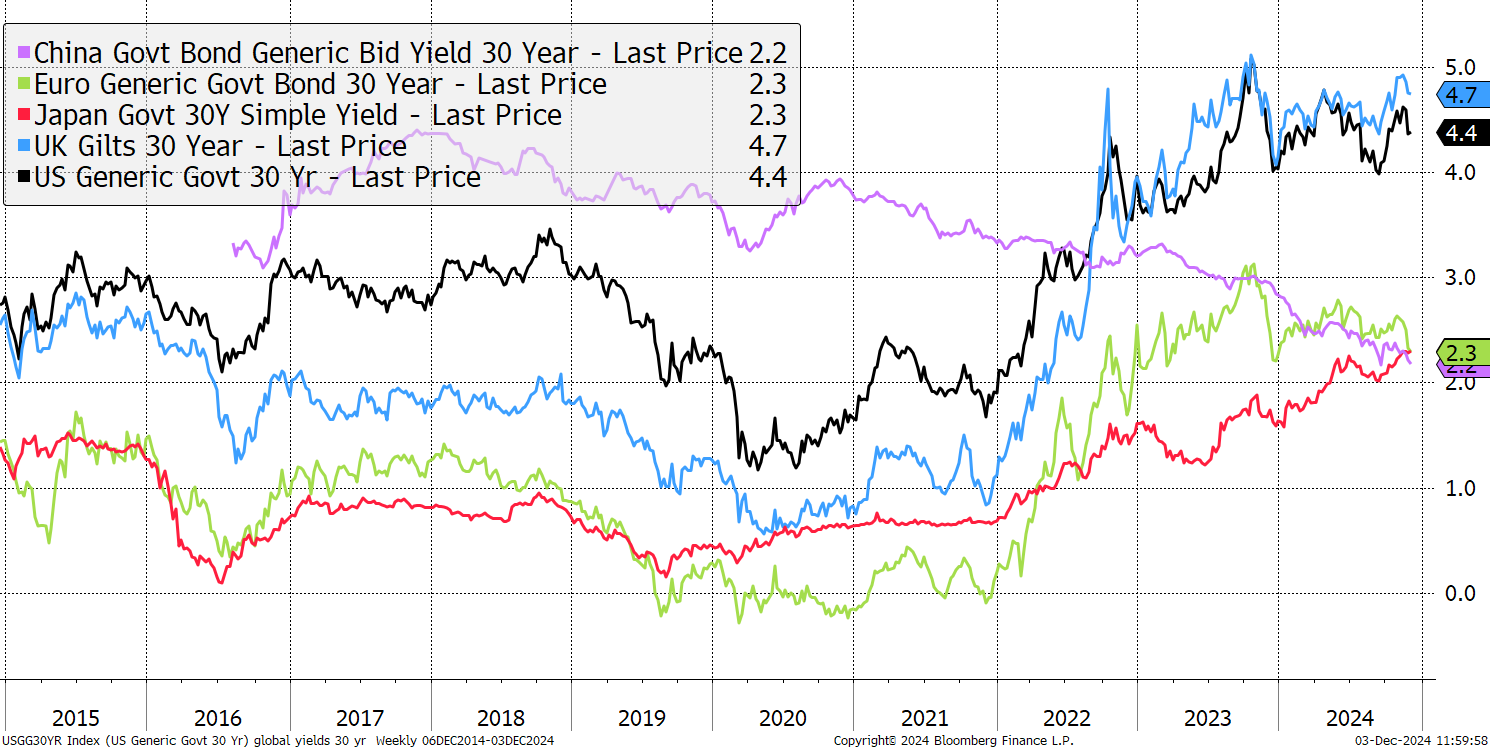

The US (black) and the UK (blue) 30-year bond yields trade closely and are headed lower from 5%. China (purple), Europe (green), and Japan (red) have met at 2.3%. These moves mean different things in different places.

Global 30-Year Bond Yields

The UK and the US have seen inflation peaks, and their economies are still expanding, although faster in the US than in the UK. Europe and China are slowing, while Japan is reflating. We are expecting rate cuts in most major economies next year, but in Japan, hikes. Japan is finally seeing rising long-term inflation expectations, not because the economy is broken but because the currency has been too cheap. It is now rising, and I wouldn’t be surprised if the US, UK and Japan meet at 3% next year. But Europe and China will no doubt be lower, and with China’s yield below Japan’s, some believe China is headed for Japanification. That means it could face a lost decade.

If global inflation is lower, it is a good time to revisit property or commercial real estate because if inflation is under control, rates will come down, and that’s good news for the sector. Yet many believe property likes inflation because the rents rise. That is true, but vacancies also rise, along with borrowing costs. The sweet spot is a high demand for space combined with cheap borrowing.

The Multi-Asset Investor is issued by ByteTree Asset Management Ltd, an appointed representative of Strata Global which is authorised and regulated by the Financial Conduct Authority. ByteTree Asset Management is a wholly owned subsidiary of ByteTree Group Ltd.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2025 ByteTree Group Ltd