Hard Assets and Gold

With gold trading at an all-time high and many commodity prices on the rise again, it is starting to feel as though the next wave of inflation is approaching. This is now being priced in by financial markets, assisted by policy uncertainty and the rise in tariffs.

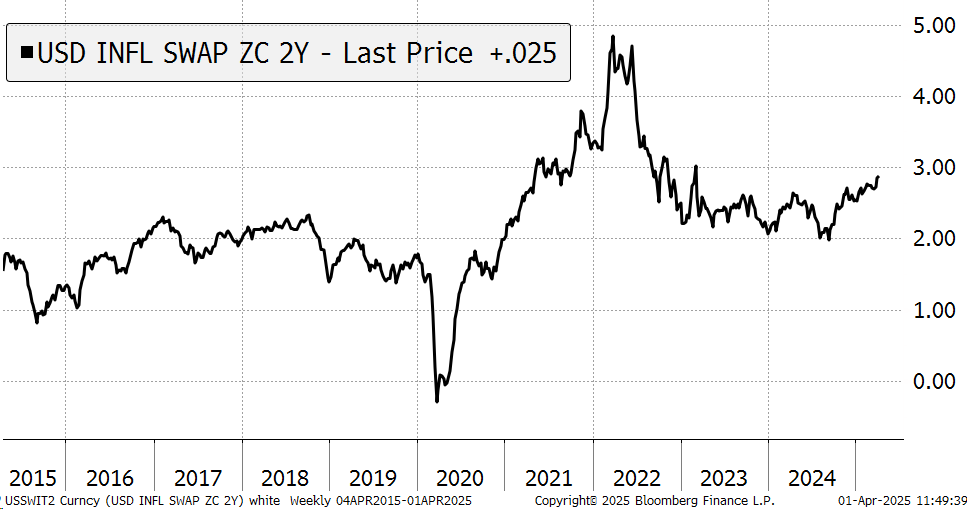

USA Two-Year Inflation Expectations

It’s a game changer for markets as the prevailing winds of 2024 have shifted. While inflation is back, bond yields remain uncertain. In the US, the DOGE initiative aims to balance the budget, making bonds more attractive. Here in the UK, the hint of austerity is perhaps a small taste of what lies ahead. Policymakers will have no choice but to cut budgets if the cost of borrowing keeps on rising. Higher inflation also weighs on bonds, which further accelerates the need for cuts in public spending. The outlook for bonds remains uncertain.

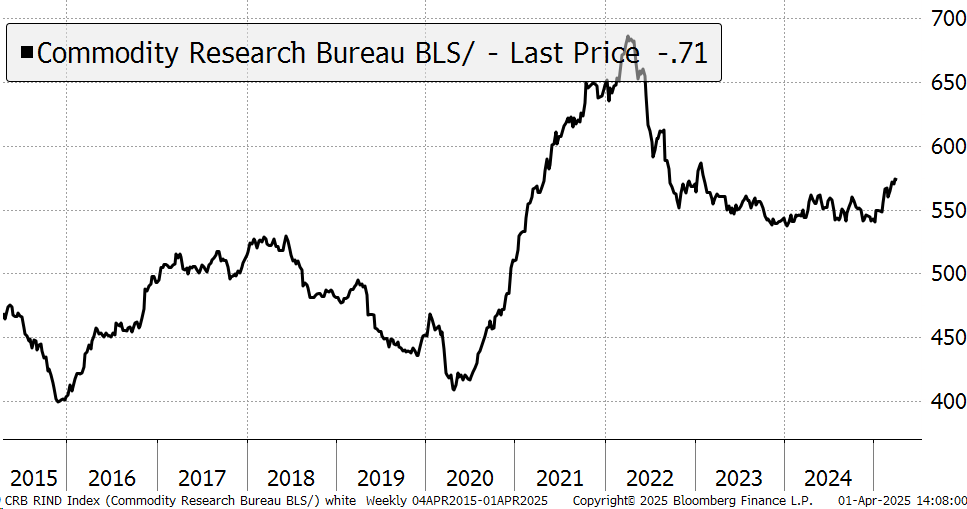

This brings us back to hard assets. The Commodities Spot Raw Industrials Index (aka the CRB RIND) is rising again, which is historically a reliable precursor before a bull market in commodities. That is, the commodities that trade off-market and provide a more reliable real-world view, as the noise from speculators is significantly reduced. A new uptrend has begun, aligning with the higher inflation expectations.

Commodities Spot Raw Industrials Index

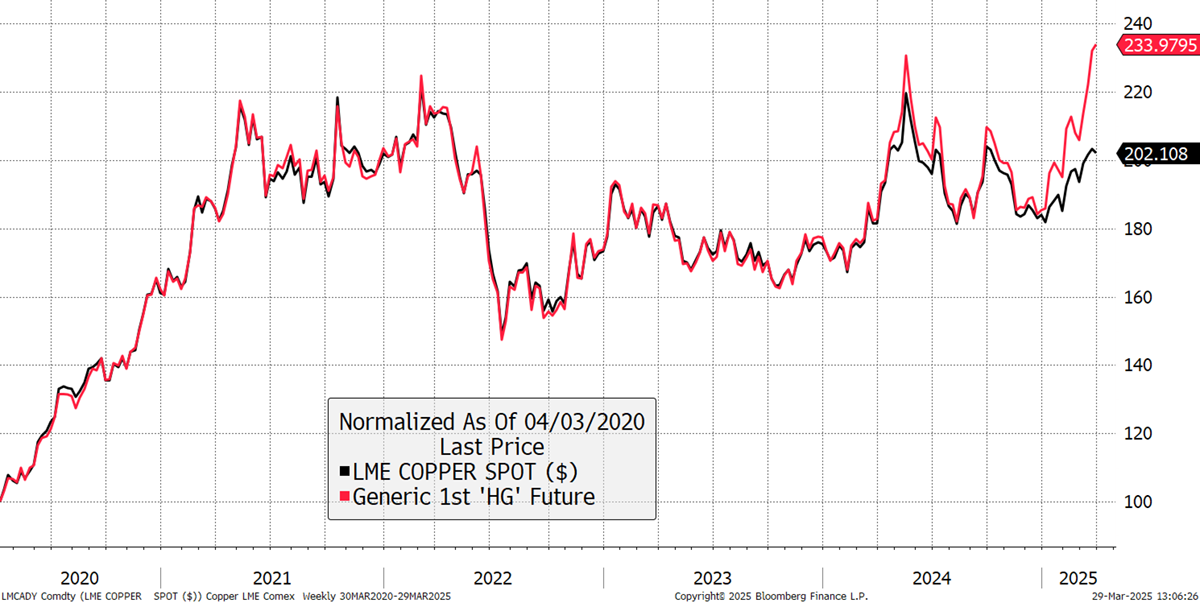

There are also anomalies in the market, such as the price of copper. US copper has surged ahead of London copper by the widest margin in years. Some attribute this to superior US growth, but a more likely explanation is the impending tariffs. This expectation has fuelled a rush to ship copper to the USA before any new trade barriers take effect.

London (black) vs US Copper Price (red)

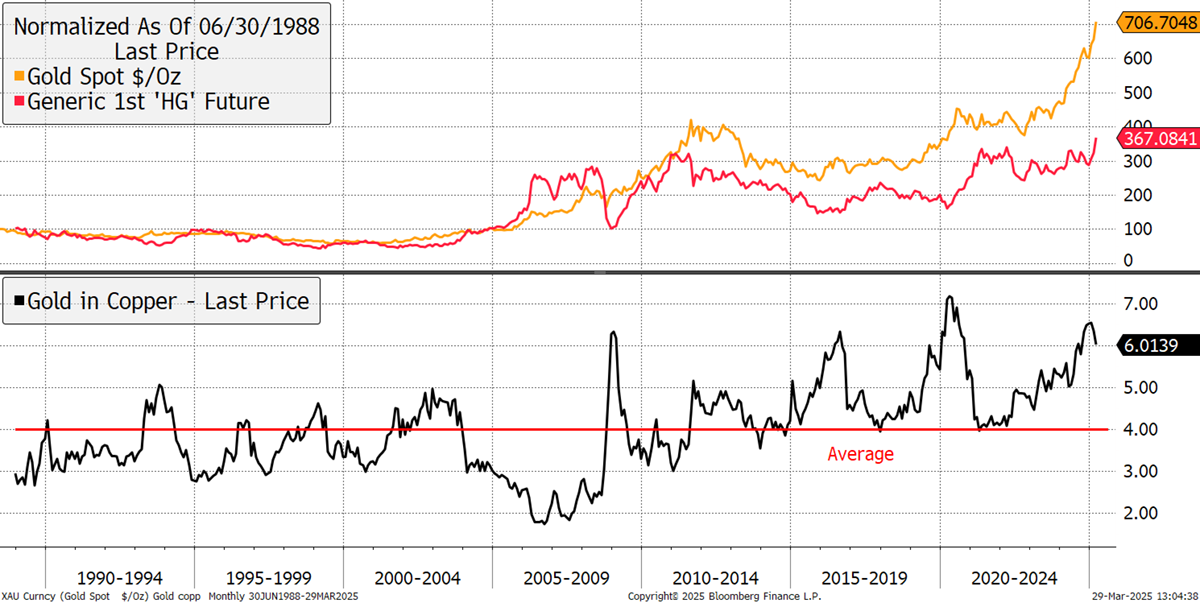

Until 2020, copper and gold had delivered similar returns, yet gold has done twice as well since. This begs the question of whether copper presents an opportunity for a catch-up trade, given that copper is cheap compared to gold and the long-term supply is constrained.

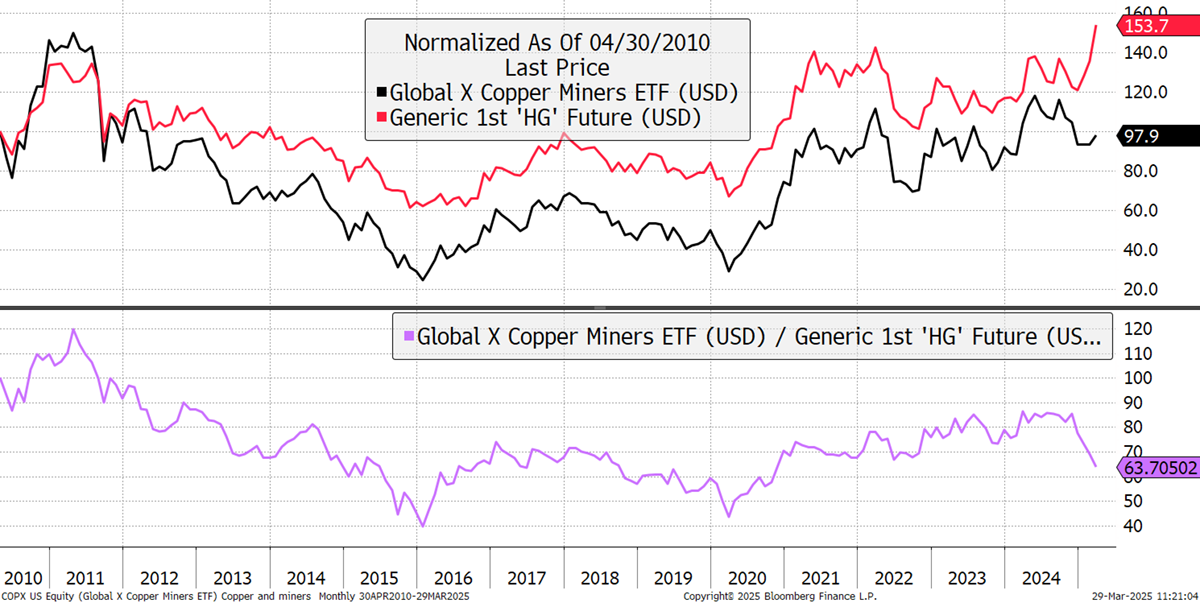

Copper versus Gold

Not only that, but copper stocks have lagged the price of copper, a similar situation to what we see between gold and the gold miners. If copper continues to rise, copper stocks are something worth looking at.

Copper and Copper Miners

Of course, we have become familiar with these relationships breaking down, and some might say the US’s strength is temporary and merely a front-running of tariffs. More likely, they are following the London (global) price, and the situation is overstated. The trouble is that these distortions have become widespread.

I am currently attending the Mining Forum Europe, which is sponsored by Denver Gold and focuses on the gold miners. There are dozens of mining companies here, with a nice backdrop of a record-high gold price. The question everyone is asking is why the mining stocks remain so cheap compared to what we might expect in the past. Answers vary, but it is clearly difficult for a gold miner to consistently grow supply. Across the industry, this has stagnated since 2018 and is unlikely to boom to levels that would threaten the gold price.

Jeroen Blokland, CEO of the Blokland Smart Multi-Asset Fund, spoke about falling productivity in the developed world and an ageing population. For example, China has 900 million workers, which will drop to 500 million by 2050. The conclusion was that governments would need to keep boosting the money supply in order to cope. Deficits will persist, and governments will need to intervene to keep a lid on the cost of borrowing. He is not the only one who thinks that quantitative easing (QE) will return before too long. Inflation, he said, will stay with us and remain volatile. This will continue to boost the value of hard assets.

John Reade, Chief Strategist of the World Gold Council, spoke about gold demand in an effort to explain the recent strength behind this spectacular bull market. High prices had led to reduced demand for jewellery, but the central banks had stepped in. Their combined reserves accounted for approximately 6% of total assets. In the 1950s and 1960s, this was closer to 60%. Even a move to 30% would support the gold price for years to come.

This move was triggered by the invasion of Ukraine and the subsequent confiscation of Russian reserves. However, even aside from this, there is a growing distrust of bond markets, which has led to the diversification of reserves. This is my Super Bull thesis, which I covered in January. It used to be the case that gold was sensitive to interest rates and thrived when yields fell. Now it seems to be the other way around, and mainstream investors are yet to notice. While the central banks are accumulating gold, many more purchases are undeclared, making the combined force a powerful force.

While this is happening, mainstream investors remain lightly positioned. They are yet to buy gold, silver, copper, and their respective miners. That makes these assets structurally undervalued, indicating that the best is yet to come.

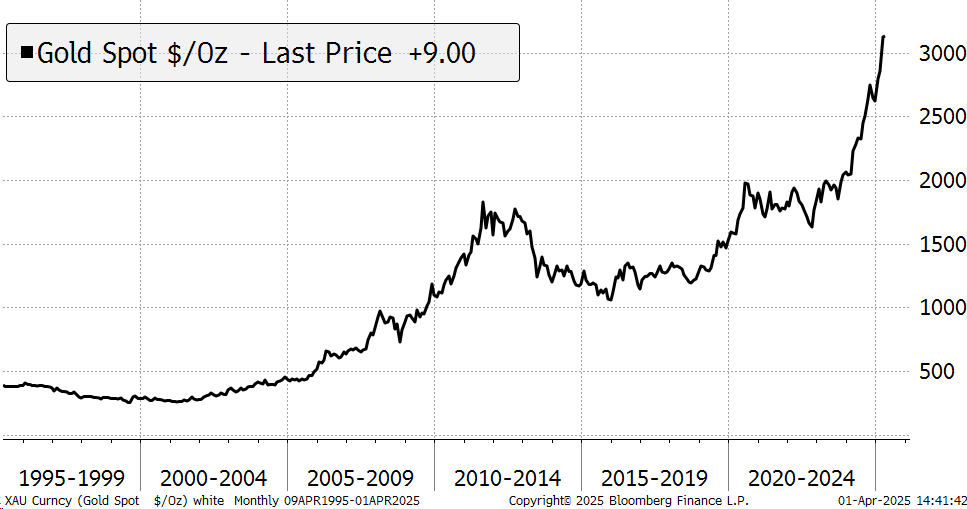

The Gold Price – Past 30 years

The Multi-Asset Investor is issued by ByteTree Asset Management Ltd, an appointed representative of Strata Global which is authorised and regulated by the Financial Conduct Authority. ByteTree Asset Management is a wholly owned subsidiary of ByteTree Group Ltd.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2025 ByteTree Group Ltd